Here’s a riddle: What do you call an automaker that makes more money selling tractors to Punjab’s wheat farmers than SUVs to Mumbai’s elites? The answer – Mahindra & Mahindra, the 78-year-old conglomerate that’s been quietly printing money through tractors while analysts drool over its Thar SUVs.

The proof lies in the profit margins: For every Rs. 100 earned from tractors, Mahindra keeps Rs. 19 as operating profit. For every Rs. 100 from SUVs? Just Rs. 9! This 2:1 margin advantage explains why tractors contributed 41% of Mahindra’s operating profits in FY25, despite generating only 35% of total revenues.

“While everyone chases electric vehicles, we’ve discovered that tractors are the ultimate ‘renewable energy’ – they run on monsoon rains and farmer optimism”, said Anish Shah (CEO) when asked about this astonishing revelation.

But here’s the real kicker: Mahindra sells a tractor every 90 seconds in India. Its 40% market share means two out of every five tractors sold nationally bear the Mahindra badge. Yet, this agricultural juggernaut remains overshadowed by its sexier SUV cousin.

So, what seems to be “driving” this agricultural juggernaut over its sexier SUV cousin?

1. Margin Superiority: The EBIT Tractor Pulls the Entire Company

The numbers tell us the brutal truth, and the first instantaneous reason for going agro:

This isn’t just about selling metal – it’s about Mahindra’s mastery of the agricultural ecosystem. Their tractors come bundled with financing (Mahindra Finance grew tractor loans 3x faster than auto loans in FY24), insurance, and a service network reaching 1,400 rural towns. As CEO Anish Shah quipped: “Our tractors don’t just till soil – they cultivate recurring revenue streams.”

The farm segment’s cash flow in H1FY25 stood at Rs. 1,555 crore – enough to fund almost half of Mahindra’s entire EV segment investments. While the industry on average registered a mere 8-11% growth in PBIT in FY25, Mahindra’s tractor division alone delivered 25**%** PBIT growth!

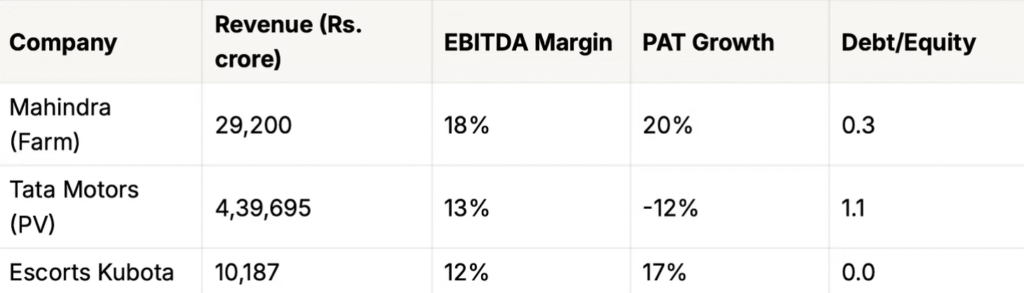

The Hidden Leverage:

Asset turnover ratio of 2.4x vs industry average of 1.8x.

Inventory turnover is 30% faster than Escorts Kubota (next best competitor).

Debt/Equity at 0.3x vs Tata Motors’ 1.1x.

This financial discipline lets Mahindra undercut competitors while maintaining premium pricing (Rs. 7.5-8 lakh, 15% premium to the next best alternative in the 30-35 BHP segment).

Yet, financial acumen only comes into the picture if the industry in itself is a conducive environment and people are buying tractors, so what does the industry have to say?

2. Cyclical Resilience: Monsoons Beat Market Volatility

While SUV sales swing with fuel prices and urban sentiment, tractors dance to nature’s rhythm. Jefferies’ analysis shows tractor demand follows predictable 4-year cycles, averaging 16% growth. After a 7.4% dip in FY23, Mahindra’s tractor sales rebounded 11% in FY24, then accelerated to 12% growth in FY25!

The secret? Built-in demand drivers:

58% of India’s workforce depends on agriculture.

45% of tractor buyers upgrade every 7-8 years.

Government MSP hikes increased farmer incomes 6% YoY.

When Cyclone Biparjoy disrupted SUV production in 2023, tractors sailed through – May 2025 domestic sales hit 38,914 units, up 10% YoY. As Rajesh Jejurikar, Farm Equipment President, noted: “When RBI hikes rates, SUV buyers pause. When IMD predicts good rains, farmers order tractors.”

“The Monsoon Multiplier” is a real phenomenon, and this is what it looks like!

1% increase in rainfall leads to 2.3% tractor sales growth.

Reservoir levels are at 86% capacity vs 74% 5-year average.

Kharif sowing up 18% YoY in Punjab/Haryana.

This agricultural leverage makes Mahindra’s tractor division the ultimate macro hedge – thriving when rural India thrives, insulated from urban slowdowns. But this is domestic – what about the rest of the world?

3. Global Gambit: The Export Game

While Mahindra dominates India with 40% tractor market share, its export strategy reveals a deeper truth: profit margins trump volume.

Mahindra’s Oja tractor’s technology, when compared to Sonalika’s Worldtrac, allows for the farmer to spend 40% less on labour (due to automation), results in 27% less fuel theft (due to telematics constantly tracking everything), and allows for 15% more yield as well!

Therefore, despite Sonalika commanding 35% of India’s tractor exports vs Mahindra’s 16%, Mahindra’s export revenue per unit is Rs. 9.2 lakh vs Sonalika’s Rs. 6.8 lakh – a 35% premium. This isn’t about selling more tractors, but smarter ones.

That doesn’t mean Mahindra doesn’t also want to sell more tractors – in fact, it’s been doing exactly that for the last decade in Brazil:

Furthermore, the BRL 100 million plant in Rio Grande do Sul (2026 launch) triples capacity to 9,000 units/year, targeting Brazil’s 2.4 million sugarcane farms. Unlike Sonalika’s focus on low-competition African markets, Mahindra’s Brazil pivot offers:

Zero import taxes across the Mercosur trade bloc.

25-40 BHP tractor demand growing 12% annually.

BRL 28,000/unit pricing (vs Rs. 7.5 lakh domestically, which is about BRL 50,000/unit).

To top it off, while Sonalika sells 65% of exports to Africa’s price-sensitive markets, Mahindra’s planting seeds in premium corridors:

US Vineyards: 5% share in 80,000-unit market via Brazil-assembled tractors.

ASEAN Rice Fields: 20% target in Thailand-led 50,000-unit segment.

Europe’s Orchards: EUR 35,000 electric tractor prototypes under FAME-III subsidies.

As CEO Anish Shah notes: “We’re not exporting tractors – we’re exporting agricultural ecosystems.” With Brazil projected to deliver US$ 450 million annual revenue by 2027, Mahindra is proving that in global farming, premium tech out-ploughs volume every harvest season.

Now that we’ve uncovered 3 of Mahindra’s magic tricks, let’s take a look at how the trick actually worked on the numbers!

Plowing Ahead: The 2027 Harvest Plan

So while Mahindra might be a fraction of the size of a giant like Tata Motors, the sheer ability to “plough” throw and be a victor in every other way makes Mahindra a more coveted stock as well, having rallied by 20% in the last year, while Tata Motors and Escorts Kubota have decline by 22% and 15% respectively!

Hence, the only thing to look forward to is the future, and we’ve jotted down 3 things that might be on the forward frontier:

New AI-driven tractor technology that is 15% more fuel efficient, 22% improvement in yields, and even more labour cost savings due to automation + an agricultural ecosystem that connects 2.1 million tractors by 2027, helping Mahindra to monetize on the data and software as well.

Mahindra intends to undertake Tractor-as-a-Service as well (Rs. 15,000/month), along with AI-powered loans that approve them within 5-minutes via facial recognition.

Coupled with the Rs. 200 crore allocation for electric tractors under FAME-III, MSP hikes of 5-12% on kharif crops and state subsidies, Mahindra might also go full-force on EV tractors.

In a market obsessed with electric vehicles and urban mobility, Mahindra’s tractor business represents something rare – a fundamentally strong, highly profitable operation hiding in plain sight.

While analysts debate SUV specs, the real value creation happens in the unglamorous world of agricultural equipment. For people willing to look beyond automotive headlines, Mahindra offers a contrarian narrative, where monsoon clouds signal profits, and tractors outmuscle SUVs in the balance sheet.